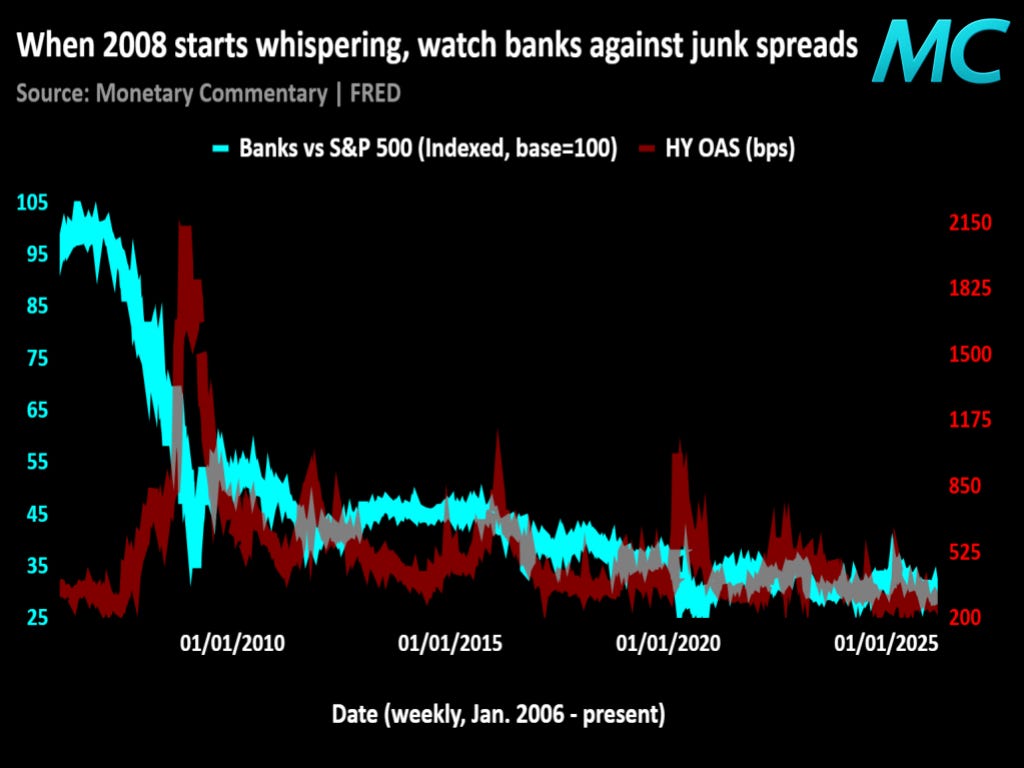

When banks crack before junk does

Bank stocks usually sniff out balance-sheet stress before high yield spreads fully price it.

Banks (XLF) versus the broad market (SPY) only really breaks hard when credit stops being repricable and starts becoming suspect collateral in investors’ minds.

High yield OAS is the cleaner confirmation because it captures the point where balance-sheet stress leaks out of equity narratives and into funding risk. When the two move together, the message is that the market is beginning to charge a premium for impaired transmission.

That is why this spread is better as an early degradation gauge than as a crash call. The real tell from here is whether bank relative performance keeps sagging even if headline spreads pause. That would mean equity is front-running a tighter credit regime before cash credit fully admits it.